According to a new market research report "Cloud Security Market by Service Type (IAM, DLP, IDS/IPS, SIEM, and Encryption), Security Type, Service Model (IaaS, PaaS, and SaaS), Deployment Type (Public, Private, and Hybrid), Organization Size, Vertical, and Region - Global Forecast to 2022", published by MarketsandMarkets™, the market size is expected to grow from USD 4.09 Billion in 2017 to USD 12.73 Billion by 2022, at a Compound Annual Growth Rate (CAGR) of 25.5%.

Browse 68 market data Tables and 71 Figures spread through 169 pages and in-depth TOC on "Cloud Security Market"

http://www.marketsandmarkets.com/Market-Reports/cloud-security-market-100018098.html

Early buyers will receive 10% customization on this report.

Cloud security helps organizations protect networks, endpoints, and applications from various malicious attacks, sophisticated cybercriminals, ransomwares, & Advanced Persistent Threats (APTs). The major forces driving the Cloud Security Market are the increased adoption of Bring Your Own Device (BYOD) & Internet of Things (IoT) trends, rise in adoption of cloud-based security services, increasing demand for cloud computing & increasing government initiatives, and emergence of smart cities. Therefore, enterprises are deploying advanced cloud security services to secure networks and endpoints from cyber threats.

The web and email security segment is expected to have the largest share in the Cloud Security Market in 2017

The web and email security segment is expected to have the largest market share and dominate the Cloud Security Market from 2017 to 2022, as more and more companies are adopting cloud-based security services to secure their business infrastructures. The major factors responsible for the growth of web and email security segment are increased usage of cloud-based web and email applications in the organizations and the need to protect these applications from advanced threats, such as ransomwares, APTs, zero-day attacks, malwares, & unauthorized accesses.

Ask for PDF Brochure @ http://www.marketsandmarkets.com/pdfdownload.asp?id=100018098

The retail vertical is expected to grow at the highest CAGR in the Cloud Security Market

The Banking, Financial Services, and Insurance (BFSI) vertical is expected to contribute to the largest market share in the Cloud Security Market. The increasing digital identities in all size of organizations and the growing trends of BYOD and IoT result in a massive growth in advanced cyberattacks, thus creating the need for adopting cloud-based security services. The retail vertical is projected to grow at the highest CAGR from 2017 to 2022 in the Cloud Security Market, because retail industries are continuously deploying cloud security services to protect customer-sensitive data and the digital identities associated with each customer stored on the cloud.

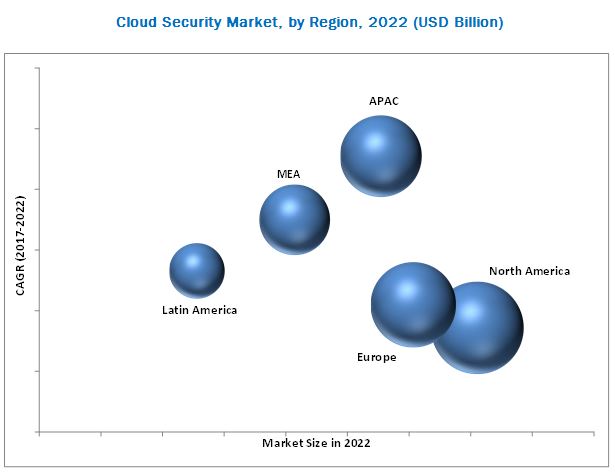

North America is expected to contribute to the largest market share, whereas Asia-Pacific (APAC) is projected to grow at the highest CAGR

North America is expected to have the largest market share and dominate the Cloud Security Market from 2017 to 2022, due to the presence of a large number of cloud security vendors across this region. APAC, on the other hand, offers potential growth opportunities in the Cloud Security Market, as there is a wide presence of small and medium enterprises in this region that is turning toward cloud security services to defend against APTs.

Inquiry before Buying @ http://www.marketsandmarkets.com/Enquiry_Before_Buying.asp?id=100018098

The major vendors in the Cloud Security Market include Trend Micro, Inc. (Tokyo, Japan), Intel Security (California, U.S.), Symantec Corporation (California, U.S.), IBM Corporation (New York, U.S.), Cisco systems (California, U.S.), CA Technologies, Inc. (New York, U.S.), CSC (Virginia, U.S.), and Fortinet, Inc. (California, U.S.).

About MarketsandMarkets™

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth niche opportunities/threats which will impact 70% to 80% of worldwide companies' revenues. Currently servicing 5000 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Our 850 fulltime analyst and SMEs at MarketsandMarkets™ are tracking global high growth markets following the "Growth Engagement Model - GEM". The GEM aims at proactive collaboration with the clients to identify new opportunities, identify most important customers, write "Attack, avoid and defend" strategies, identify sources of incremental revenues for both the company and its competitors. MarketsandMarkets™ now coming up with 1,500 MicroQuadrants (Positioning top players across leaders, emerging companies, innovators, strategic players) annually in high growth emerging segments. MarketsandMarkets™ is determined to benefit more than 10,000 companies this year for their revenue planning and help them take their innovations/disruptions early to the market by providing them research ahead of the curve.

MarketsandMarkets's flagship competitive intelligence and market research platform, "RT" connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact:

Mr. Rohan

MarketsandMarkets™

701 Pike Street

Suite 2175, Seattle,

WA 98101, United States

Tel: +1-888-600-6441

Email: sales@marketsandmarkets.com

Browse 68 market data Tables and 71 Figures spread through 169 pages and in-depth TOC on "Cloud Security Market"

http://www.marketsandmarkets.com/Market-Reports/cloud-security-market-100018098.html

Early buyers will receive 10% customization on this report.

Cloud security helps organizations protect networks, endpoints, and applications from various malicious attacks, sophisticated cybercriminals, ransomwares, & Advanced Persistent Threats (APTs). The major forces driving the Cloud Security Market are the increased adoption of Bring Your Own Device (BYOD) & Internet of Things (IoT) trends, rise in adoption of cloud-based security services, increasing demand for cloud computing & increasing government initiatives, and emergence of smart cities. Therefore, enterprises are deploying advanced cloud security services to secure networks and endpoints from cyber threats.

The web and email security segment is expected to have the largest share in the Cloud Security Market in 2017

The web and email security segment is expected to have the largest market share and dominate the Cloud Security Market from 2017 to 2022, as more and more companies are adopting cloud-based security services to secure their business infrastructures. The major factors responsible for the growth of web and email security segment are increased usage of cloud-based web and email applications in the organizations and the need to protect these applications from advanced threats, such as ransomwares, APTs, zero-day attacks, malwares, & unauthorized accesses.

Ask for PDF Brochure @ http://www.marketsandmarkets.com/pdfdownload.asp?id=100018098

The retail vertical is expected to grow at the highest CAGR in the Cloud Security Market

The Banking, Financial Services, and Insurance (BFSI) vertical is expected to contribute to the largest market share in the Cloud Security Market. The increasing digital identities in all size of organizations and the growing trends of BYOD and IoT result in a massive growth in advanced cyberattacks, thus creating the need for adopting cloud-based security services. The retail vertical is projected to grow at the highest CAGR from 2017 to 2022 in the Cloud Security Market, because retail industries are continuously deploying cloud security services to protect customer-sensitive data and the digital identities associated with each customer stored on the cloud.

North America is expected to contribute to the largest market share, whereas Asia-Pacific (APAC) is projected to grow at the highest CAGR

North America is expected to have the largest market share and dominate the Cloud Security Market from 2017 to 2022, due to the presence of a large number of cloud security vendors across this region. APAC, on the other hand, offers potential growth opportunities in the Cloud Security Market, as there is a wide presence of small and medium enterprises in this region that is turning toward cloud security services to defend against APTs.

Inquiry before Buying @ http://www.marketsandmarkets.com/Enquiry_Before_Buying.asp?id=100018098

The major vendors in the Cloud Security Market include Trend Micro, Inc. (Tokyo, Japan), Intel Security (California, U.S.), Symantec Corporation (California, U.S.), IBM Corporation (New York, U.S.), Cisco systems (California, U.S.), CA Technologies, Inc. (New York, U.S.), CSC (Virginia, U.S.), and Fortinet, Inc. (California, U.S.).

About MarketsandMarkets™

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth niche opportunities/threats which will impact 70% to 80% of worldwide companies' revenues. Currently servicing 5000 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Our 850 fulltime analyst and SMEs at MarketsandMarkets™ are tracking global high growth markets following the "Growth Engagement Model - GEM". The GEM aims at proactive collaboration with the clients to identify new opportunities, identify most important customers, write "Attack, avoid and defend" strategies, identify sources of incremental revenues for both the company and its competitors. MarketsandMarkets™ now coming up with 1,500 MicroQuadrants (Positioning top players across leaders, emerging companies, innovators, strategic players) annually in high growth emerging segments. MarketsandMarkets™ is determined to benefit more than 10,000 companies this year for their revenue planning and help them take their innovations/disruptions early to the market by providing them research ahead of the curve.

MarketsandMarkets's flagship competitive intelligence and market research platform, "RT" connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact:

Mr. Rohan

MarketsandMarkets™

701 Pike Street

Suite 2175, Seattle,

WA 98101, United States

Tel: +1-888-600-6441

Email: sales@marketsandmarkets.com